Every business spends money. But not all spending is the same.

If you're a new entrepreneur, startup founder, or business student, understanding where your money goes is one of the most important skills you can develop. Yet most accounting textbooks make it feel like rocket science.

Here's the truth: once you understand the types of business costs, managing your money becomes dramatically easier. You'll make smarter decisions, avoid costly mistakes, and know exactly where to cut expenses when times get tough.

In this guide, we break down every major type of business cost in plain English, with real-world examples that actually make sense.

Quick Answer: What Are the Types of Business Costs?

The main types of business costs are: fixed costs, variable costs, semi-variable costs, direct costs, indirect costs, operating expenses (OPEX), capital expenditures (CAPEX), overhead costs, sunk costs, opportunity costs, explicit costs, implicit costs, and marginal costs. Each category helps businesses track, control, and optimize their financial performance.

Table of Contents

- Why Understanding Business Costs Matters

- Fixed vs Variable Costs

- Semi-Variable Costs

- Direct and Indirect Costs

- Overhead Costs for Small Business

- OPEX vs CAPEX

- Sunk Costs vs Opportunity Costs

- Explicit and Implicit Costs

- Marginal Cost of Production

- Cost Comparison Table

- FAQ

- Conclusion

1. Why Understanding Business Costs Matters

Business costs directly affect your profit. Simple as that.

If you don't know what type of cost you're dealing with, you can't control it properly. You might cut the wrong expense and hurt your growth, or overspend in areas that don't actually drive revenue.

Understanding cost categories also helps you:

- Price your products correctly

- Prepare accurate financial statements

- Apply for loans or attract investors

- Plan for seasonal changes in revenue

- Make smarter hiring and expansion decisions

Now let's break down each type of business cost one by one.

2. Fixed vs Variable Costs

This is the most fundamental distinction in business finance.

Fixed Costs

Fixed costs are expenses that stay the same regardless of how much you produce or sell.

It doesn't matter if you sell 10 units or 10,000 units; your fixed costs remain constant.

Common fixed cost examples:

- Office or store rent

- Employee salaries (permanent staff)

- Insurance premiums

- Software subscriptions (monthly flat fees)

- Loan repayments

Example: A bakery pays $2,000 per month in rent. Whether they bake 100 loaves or 1,000 loaves, that rent bill never changes.

Variable Costs

Variable costs change in direct proportion to your production or sales volume.

More output means more variable costs. Less output means fewer variable costs.

Common variable cost examples:

- Raw materials and ingredients

- Packaging costs

- Shipping and delivery fees

- Sales commissions

- Payment processing fees

Example: That same bakery spends $0.50 on flour, butter, and packaging per loaf. If they bake 500 loaves, variable costs are $250. If they bake 1,000 loaves, costs double to $500.

Why This Distinction Matters

Knowing which costs are fixed and which are variable helps you calculate your break-even point: the exact number of sales you need to cover all your costs.

3. Semi-Variable Costs in Accounting

Semi-variable costs (also called mixed costs) have both a fixed component and a variable component.

They're fixed up to a certain level of activity, then increase as production grows.

Real-world examples of semi-variable costs:

- Electricity bills: You pay a base connection fee (fixed) plus usage charges (variable)

- Phone plans: A base monthly rate plus per-minute or per-data overage charges

- Salesperson pay: A base salary (fixed) plus commission on sales (variable)

Example: A small logistics company pays a base fee of $500/month for their fleet management software, plus $2 per delivery tracked. At 300 deliveries, their total cost is $1,100.

Semi-variable costs require you to split them into their two components when doing proper accounting analysis.

4. Direct and Indirect Costs

Direct Costs

Direct costs can be traced directly to a specific product, project, or service. They are the costs that exist because of that specific thing you're producing.

Direct cost examples:

- Wood used to make furniture

- Labor hours spent on a specific client project

- Fabric used to sew a garment

- Ingredients in a specific menu item

Indirect Costs Examples

Indirect costs (also called overhead) cannot be tied to a single product or service. They support the overall business operation.

Indirect cost examples:

- Office cleaning services

- Accounting and legal fees

- General manager's salary

- Marketing campaigns for the entire brand

Key difference: If a cost disappears when you stop making a specific product, it's direct. If it stays regardless, it's indirect.

5. Overhead Costs for Small Business

Overhead costs are the ongoing expenses required to run your business, separate from the direct cost of making your product or delivering your service. For small businesses, especially keeping overhead low is critical to staying profitable.

Types of Overhead Costs

Overhead Category Examples:

- Fixed Overhead- Rent: insurance, salaried admin staff, variable Overhead- Utility bills, office supplies.

- Semi-Variable Overhead: Phone plans, maintenance costs

How to Calculate Overhead Rate

Use this simple formula:

Overhead Rate = (Total Overhead Costs ÷ Total Direct Costs) × 100

Example: If your monthly overhead is $3,000 and your direct costs are $10,000, your overhead rate is 30%. This means for every dollar you spend directly on production, you spend 30 cents just keeping the business running.

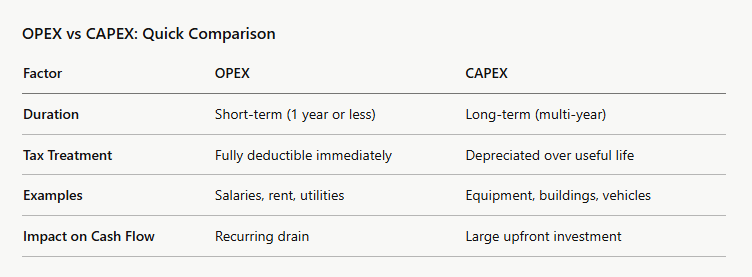

6. Operating Expenses vs Capital Expenditures

This distinction is especially important for tax purposes and financial reporting.

Operating Expenses (OPEX)

OPEX are day-to-day costs required to run the business. These are fully deducted in the year they occur.

OPEX examples:

- Employee wages

- Rent and utilities

- Marketing and advertising

- Software subscriptions

- Office supplies

Capital Expenditures (CAPEX)

CAPEX are investments in long-term assets that provide value over multiple years. Instead of being fully expensed immediately, they are depreciated over time.

CAPEX examples:

- Purchasing machinery or equipment

- Buying a company vehicle

- Building or renovating a facility

- Acquiring patents or software licenses

OPEX vs CAPEX: Quick Comparison

7. Sunk Costs vs Opportunity Costs

These two cost types are more about decision-making than bookkeeping. But they're just as important.

Sunk Costs

A sunk cost is money already spent that cannot be recovered, regardless of future decisions.

The golden rule: never let sunk costs drive future decisions.

Example: You spend $5,000 developing a product that's clearly failing. The $5,000 is gone either way. The question is whether you spend another $5,000 to continue or cut your losses.

Many business owners fall into the sunk cost fallacy: continuing a bad investment just because they've already spent money on it. Don't do this.

Opportunity Costs

An opportunity cost is the value of the next best alternative you give up when making a decision.

It's not a line item on your financial statement. But it's very real.

Example: You have $20,000 and choose to invest it in new inventory. The opportunity cost is the return you could have earned by investing that $20,000 elsewhere, say in stocks, marketing, or new equipment.

Always ask: "What am I giving up by making this choice?"

8. Explicit and Implicit Costs

Explicit Costs

Explicit costs are direct, out-of-pocket payments a business makes. They show up clearly in your accounting records.

Examples:

- Paying an employee's salary

- Buying raw materials

- Paying your monthly rent

Implicit Costs

Implicit costs are the hidden costs of using resources you already own. They don't involve a direct payment but represent real economic value.

Examples:

- The salary you could have earned working elsewhere instead of running your own business

- The rent income you forgot by using your own building for your business

Why this matters for entrepreneurs: When calculating true economic profit (not just accounting profit), you must factor in implicit costs. Many small business owners appear profitable on paper but are actually earning less than they would in a regular job.

9. Marginal Cost of Production

Marginal cost is the cost of producing one additional unit of a product or service.

Formula: Marginal Cost = Change in Total Cost ÷ Change in Quantity

Example: Your bakery currently produces 100 loaves at a total cost of $300. Adding one more loaf brings total costs to $302.50.

Marginal cost = $2.50 per additional loaf.

Why Marginal Cost Matters

- If your selling price is higher than your marginal cost, producing more is profitable.

- If your selling price falls below your marginal cost, every additional unit loses money.

Marginal cost thinking is especially important for pricing decisions, scaling production, and understanding economies of scale.

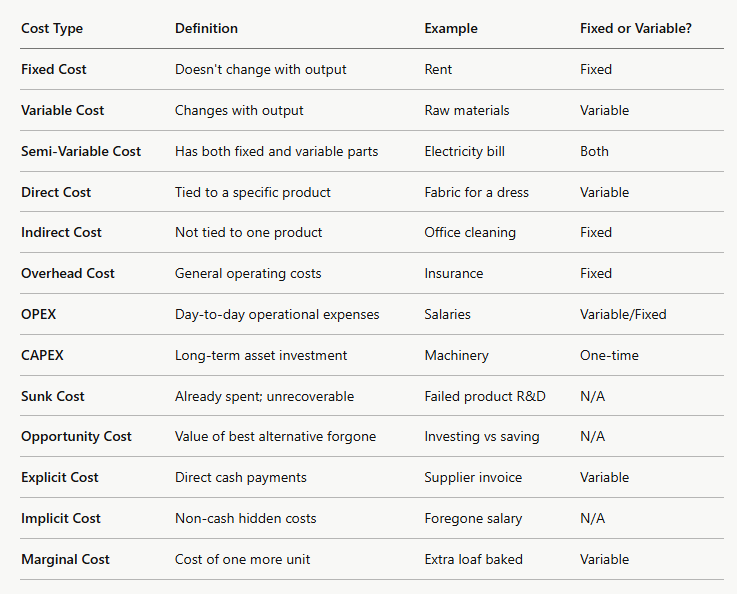

10. Cost Comparison Table

11. FAQ Section

What is the difference between fixed and variable costs?

Fixed costs remain constant regardless of production volume (like rent), while variable costs increase or decrease directly with the amount you produce or sell (like raw materials).

What are direct and indirect costs in business?

Direct costs are expenses directly tied to producing a specific product or service (like ingredients in food). Indirect costs support the overall business and cannot be traced to one product (like office rent or accounting fees).

What is the difference between OPEX and CAPEX?

OPEX (operating expenses) are recurring day-to-day costs like salaries and utilities. CAPEX (capital expenditures) are investments in long-term assets like equipment or buildings, which are depreciated over time rather than fully expensed immediately.

What is a sunk cost and why should you ignore it?

A sunk cost is money already spent that cannot be recovered. Business owners should ignore sunk costs when making future decisions because the money is gone regardless of what happens next. Continuing a bad investment just because you've already spent money on it is called the sunk cost fallacy.

What are overhead costs for a small business?

Overhead costs are ongoing expenses required to keep the business running, not tied to a specific product. Examples include rent, utilities, insurance, and administrative salaries. Keeping overhead low is critical for small business profitability.

What is marginal cost of production?

Marginal cost is the cost of producing one additional unit of output. It is calculated by dividing the change in total cost by the change in quantity. It helps businesses decide whether producing more units is profitable.

Conclusion

Understanding the types of business costs is not just an accounting exercise. It's one of the most practical skills any entrepreneur or business student can develop.

Here's a quick recap of what we covered:

- Fixed costs stay constant; variable costs change with output

- Semi-variable costs have both a fixed base and a variable component

- Direct costs link to specific products; indirect costs support the whole business

- Overhead costs are general operating expenses every business carries

- OPEX covers day-to-day operations; CAPEX covers long-term asset investments

- Sunk costs are gone forever; never let them drive your decisions

- Opportunity costs remind you what you give up with every choice you make

- Explicit costs are visible cash payments; implicit costs are hidden economic losses

- Marginal cost tells you whether producing one more unit is worth it

Once you can look at any expense and instantly know which category it belongs to, your financial decision-making will sharpen dramatically.

Start small. Review your own business expenses this week and label each one using the categories from this guide. You'll be surprised how quickly the picture becomes clearer.