Every business spends money. But not all spending works the same way.

Some costs show up every month like clockwork, whether you sell 10 units or 10,000. Others grow and shrink right alongside your sales volume. Knowing the difference between fixed costs vs variable costs is one of the most fundamental skills in business finance.

And yet, most beginner guides treat this topic like a dry accounting lesson. This guide does the opposite.

By the end, you will know exactly what each cost type means, how to identify them in your own business, and how to use that knowledge to make smarter pricing and profitability decisions. Whether you are a student, a new manager, or someone just starting a small business, this guide was written for you.

Quick Answer: Fixed Costs vs Variable Costs

Fixed costs are business expenses that stay the same regardless of how much you produce or sell. Variable costs change in direct proportion to your output or sales volume. Together, they make up your total cost of running a business.

Table of Contents

- What Are Fixed Costs? (Definition + Examples)

- What Are Variable Costs? (Definition + Examples)

- Fixed vs Variable Costs: Side-by-Side Comparison

- Mixed Costs (Semi-Variable Costs) Explained

- How Cost Behavior Affects Business Decisions

- Break-Even Analysis: Using Both Costs Together

- Operating Expenses vs COGS: How They Relate

- Total Cost Calculation: A Simple Formula

- Real-World Examples by Industry

- FAQ

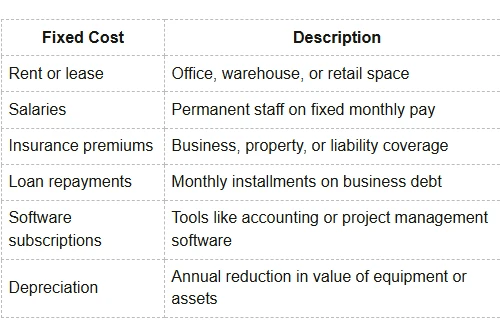

1. What Are Fixed Costs? (Definition + Examples)

Fixed Cost Definition

A fixed cost is any business expense that does not change with the level of production or sales activity. You pay it whether your output is zero or at full capacity.

Think of it as the price of keeping the lights on and the doors open.

Fixed costs are also called period costs because they are tied to a time period, not a unit of production. They are predictable, which makes budgeting easier. But they also create financial pressure during slow seasons because they never go away.

Common Fixed Cost Examples

Key characteristic: Fixed costs per unit actually decrease as you produce more. If your monthly rent is $2,000 and you make 100 products, the fixed cost per unit is $20. If you make 1,000 products, it drops to $2 per unit. This is the logic behind economies of scale.

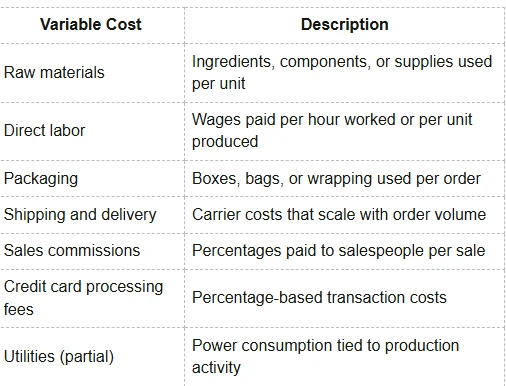

2. What Are Variable Costs? (Definition + Examples)

Variable Cost Definition

A variable cost is a business expense that increases or decreases in direct proportion to your production volume or sales output.

The more you make or sell, the higher your variable costs. The less you make, the lower they go. At zero production, variable costs are essentially zero.

Variable costs are directly tied to your Cost of Goods Sold (COGS) and represent the actual resources consumed to deliver your product or service.

Common Variable Cost Examples

Key characteristic: Variable cost per unit tends to stay constant. If it costs $5 in materials to make one product, it costs $500 to make 100. The per-unit cost does not change (unless you get bulk discounts, which then introduces a stepped or semi-variable element.

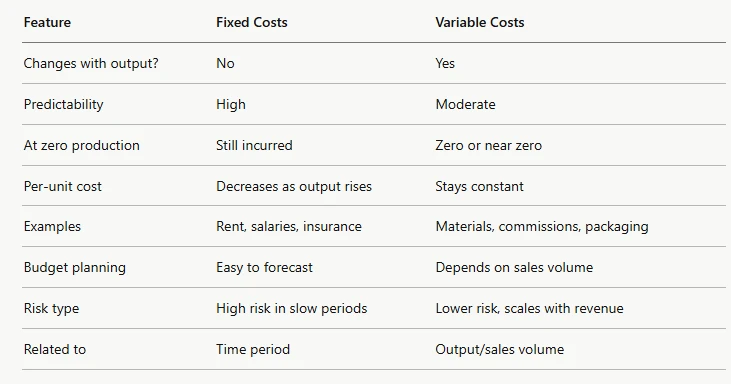

3. Fixed vs Variable Costs: Side-by-Side Comparison

The bottom line: Fixed costs give you stability and predictability. Variable costs give you flexibility because they naturally contract when business slows down.

4. Mixed Costs (Semi-Variable Costs) Explained

Not every business expense fits cleanly into one box. Some costs have both a fixed and a variable component. These are called mixed costs or semi-variable costs.

What Are Mixed Costs?

A mixed cost (also called a semi-variable cost) has a fixed base amount that is always incurred, plus a variable portion that increases with activity or usage.

A classic example is a cell phone plan with a $30 base fee plus $0.10 per extra minute. The $30 is fixed. The per-minute charge is variable.

Real-World Mixed Cost Examples

Electricity bill: A business pays a baseline connection fee every month (fixed). On top of that, the cost increases based on how much power the machinery uses (variable).

Sales rep compensation: A sales manager earns a base salary of $3,000 per month (fixed) plus a commission on every sale closed (variable).

Internet or phone service: A flat monthly rate plus overage charges for data or usage beyond the plan limit.

Why Mixed Costs Matter

If you classify a mixed cost entirely as fixed, you will overestimate your profitability during high-volume months. If you classify it entirely as variable, you will underestimate costs during slow months. Separating the two components using methods like the high-low method helps you build more accurate forecasts.

5. How Cost Behavior Affects Business Decisions

Understanding cost behavior is not just accounting theory. It directly shapes how you price products, plan production, and manage profitability.

Here is how each cost type influences key business decisions:

Pricing strategy: Your variable cost per unit sets your absolute floor for pricing. You can never sell below variable cost for long without losing money on every unit.

Scaling decisions: Because fixed costs are spread across more units as you grow, scaling up production generally improves your profit margins, as long as variable costs stay in check.

Break-even planning: Knowing both cost types lets you calculate the minimum sales volume needed to cover all costs and start generating profit.

Cost-cutting during downturns: In a slow period, you cannot quickly reduce fixed costs like rent or salaried staff. But you can reduce variable costs by ordering fewer materials or pausing commissions. This is why high fixed-cost businesses (like airlines or hotels) face severe losses during demand drops.

Outsourcing vs in-house decisions: Hiring a full-time employee adds a fixed cost. Hiring a freelancer turns that into a variable cost. The right choice depends on how predictable and consistent the workload is.

6. Break-Even Analysis: Using Both Costs Together

Break-Even Analysis Formula

Break-even analysis tells you exactly how many units you need to sell to cover all your costs. At the break-even point, you are making zero profit but also zero loss.

The formula:

Break-Even Point (Units) = Fixed Costs ÷ (Selling Price per Unit − Variable Cost per Unit)

The denominator (Selling Price − Variable Cost per Unit) is called the contribution margin per unit. It tells you how much each sale contributes toward covering your fixed costs.

Step-by-Step Break-Even Calculation

- List all fixed costs: Add up monthly rent, salaries, insurance, subscriptions, etc.

- Calculate variable cost per unit: Materials + direct labor + packaging per single unit.

- Set your selling price per unit.

- Calculate contribution margin: Selling price − variable cost per unit.

- Divide fixed costs by contribution margin.

Practical Example

Suppose you run a candle business:

- Monthly fixed costs: $2,000 (rent + utilities + software)

- Variable cost per candle: $4 (wax + wick + jar + label)

- Selling price per candle: $14

Contribution margin: $14 − $4 = $10 per candle

Break-even point: $2,000 ÷ $10 = 200 candles per month

You need to sell 200 candles before you earn a single dollar of profit. Every candle sold after that contributes $10 directly to profit.

7. Operating Expenses vs COGS: How They Relate

Many beginners confuse operating expenses with cost of goods sold. Here is a clean breakdown.

Cost of Goods Sold (COGS): Includes the direct costs of producing what you sell. This covers raw materials, direct labor, and manufacturing overhead. Variable costs are the heart of COGS.

Operating Expenses (OpEx): Includes costs needed to run the business outside of direct production. This covers rent, marketing, administrative salaries, insurance, and depreciation. Fixed costs are primarily found here.

Both categories contribute to your total cost structure. Your gross profit is Revenue − COGS. Your operating profit is Gross Profit − Operating Expenses.

Understanding which costs belong where helps you read a profit and loss statement correctly and identify where to cut when margins are tight.

8. Total Cost Calculation

Total Cost Formula

Total Cost = Total Fixed Costs + Total Variable Costs

Or expressed differently:

Total Cost = Fixed Costs + (Variable Cost per Unit × Number of Units)

Example

A small bakery has:

- Fixed costs: $3,000/month

- Variable cost per loaf: $1.50

- Production volume: 1,000 loaves/month

Total Cost = $3,000 + ($1.50 × 1,000) = $3,000 + $1,500 = $4,500/month

If they bake 2,000 loaves instead:

Total Cost = $3,000 + ($1.50 × 2,000) = $3,000 + $3,000 = $6,000/month

Notice the fixed cost stays at $3,000 while total cost grows due to higher variable costs.

9. Real-World Examples by Industry

Retail Business (Online Store)

- Fixed costs: Store subscription, warehouse lease, salaried staff

- Variable costs: Product cost per item, shipping per order, payment processing fees

Restaurant

- Fixed costs: Rent, kitchen equipment leases, manager salary

- Variable costs: Food ingredients, disposable supplies, part-time server wages

SaaS Company (Software)

- Fixed costs: Server infrastructure, developer salaries, office space

- Variable costs: Customer support costs per ticket, payment gateway fees per transaction

Freelancer / Consultant

- Fixed costs: Website hosting, software tools, professional memberships

- Variable costs: Project-specific tools, subcontractors hired per client, travel per engagement

10. Frequently Asked Questions

Q1: What is the main difference between fixed costs and variable costs? Fixed costs stay the same regardless of how much you produce or sell. Variable costs change in direct proportion to your production or sales volume. Rent is fixed. Raw materials are variable.

Q2: Are salaries fixed or variable costs? Regular employee salaries are fixed costs because they are paid monthly regardless of output. Hourly wages for production workers or freelance pay per project are variable costs because they scale with activity.

Q3: What are examples of mixed costs in a business? Mixed costs include electricity bills (base fee + usage charge), salesperson compensation (base salary + commission), and cloud storage plans (flat monthly rate + per-gigabyte overage fees).

Q4: How do fixed and variable costs affect profit margins? As production volume increases, fixed costs are spread across more units, lowering the per-unit fixed cost and improving your profit margin. Variable costs per unit remain constant, so managing them directly affects your contribution margin on every single sale.

Q5: What is the break-even analysis formula? Break-Even Point (Units) = Fixed Costs ÷ (Selling Price per Unit − Variable Cost per Unit). This tells you the minimum sales volume needed to cover all costs before earning any profit.

Q6: Why is it important to separate fixed and variable costs? Separating these costs helps you set accurate prices, forecast profits at different sales volumes, plan break-even points, identify where to cut costs during downturns, and make smarter decisions about scaling or outsourcing.

Conclusion

Understanding fixed costs vs variable costs is not just a lesson for accounting class. It is the foundation of every smart financial decision a business owner or manager makes.

Fixed costs give you stability and scale better as volume grows. Variable costs give you flexibility and move in sync with your sales. Mixed costs blend both, and knowing how to split them keeps your forecasts honest.

With this framework, you can calculate your break-even point, set prices that actually protect your margins, and build a business model that stays profitable as you grow.

Start by listing every expense in your business and sorting it into these two categories. That single exercise will give you more financial clarity than almost any other tool available to you.

Found this guide helpful? Share it with a fellow business owner or student who is just getting started with business finance.